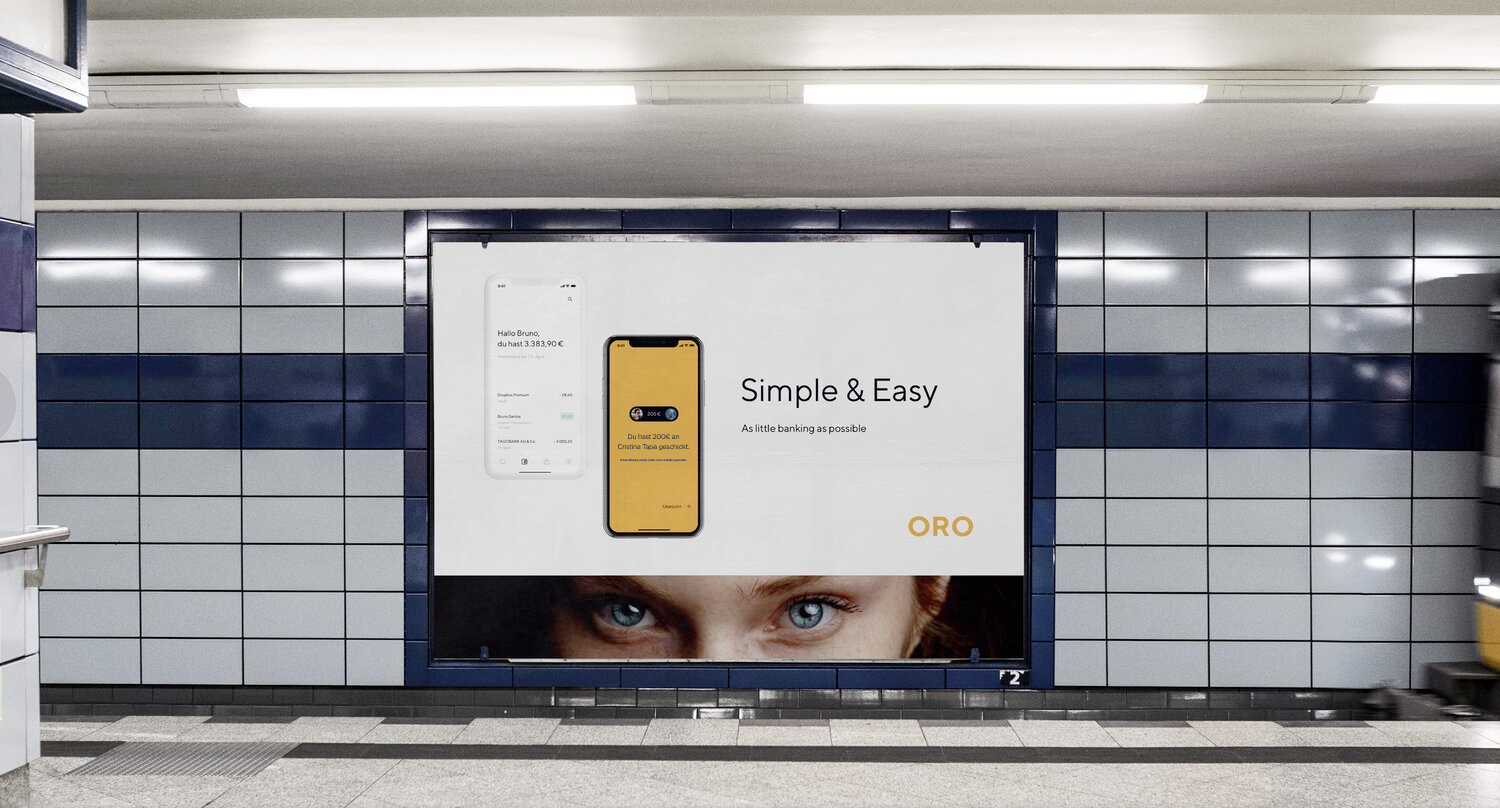

Oro was a digital financIAL Education/management app created for Commerzbank AG by a small, collaborative team at Neugelb Studios in Berlin, Germany.

When I joined the agency as Senior Visual Designer in 2020, every incumbent bank had a digital solution for covering the basic needs of retail clients… but there was no digital service [within the German market] that supported users to both understand their respective financial situation and receive personalized recommendations on how to improve it.

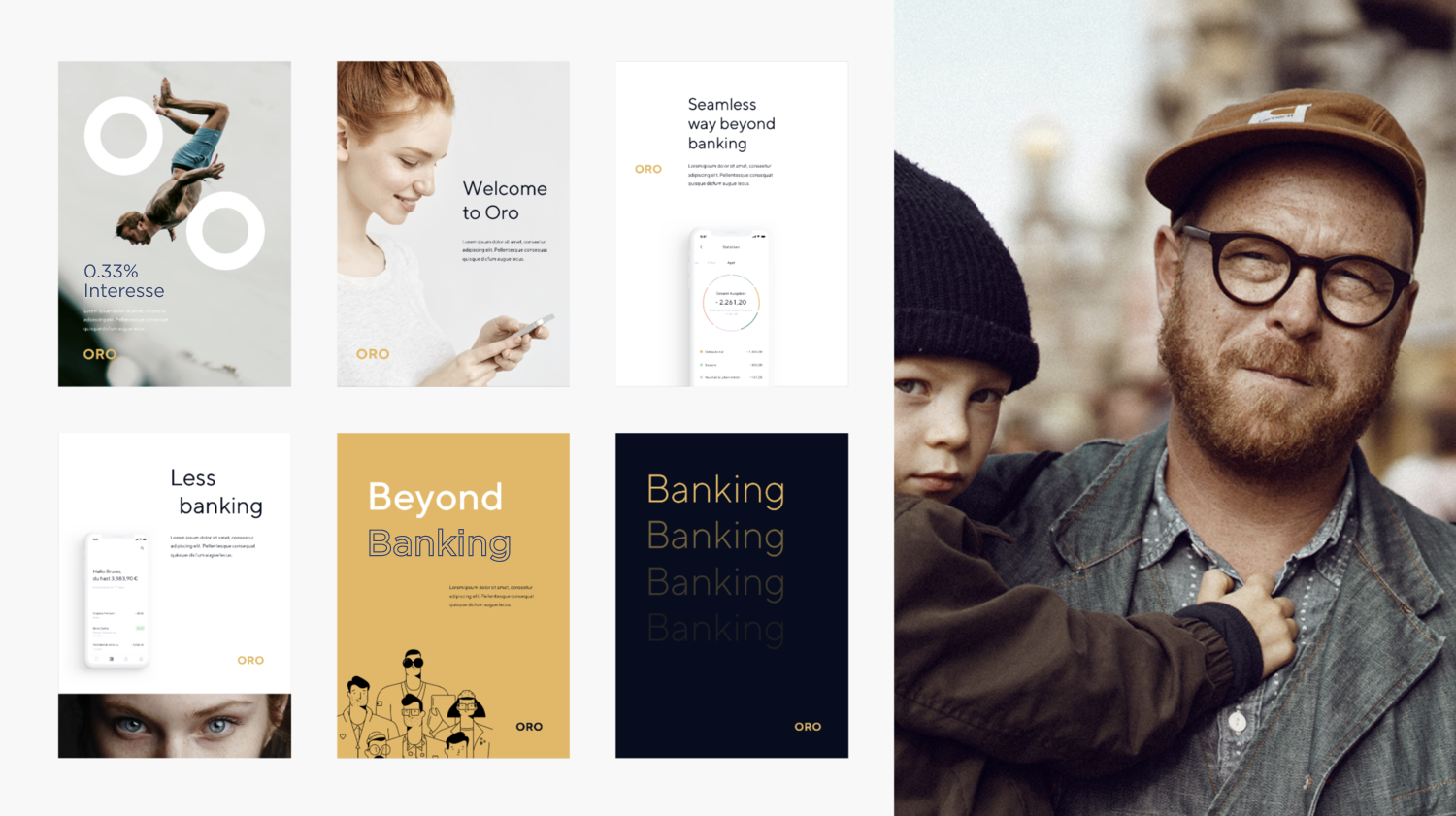

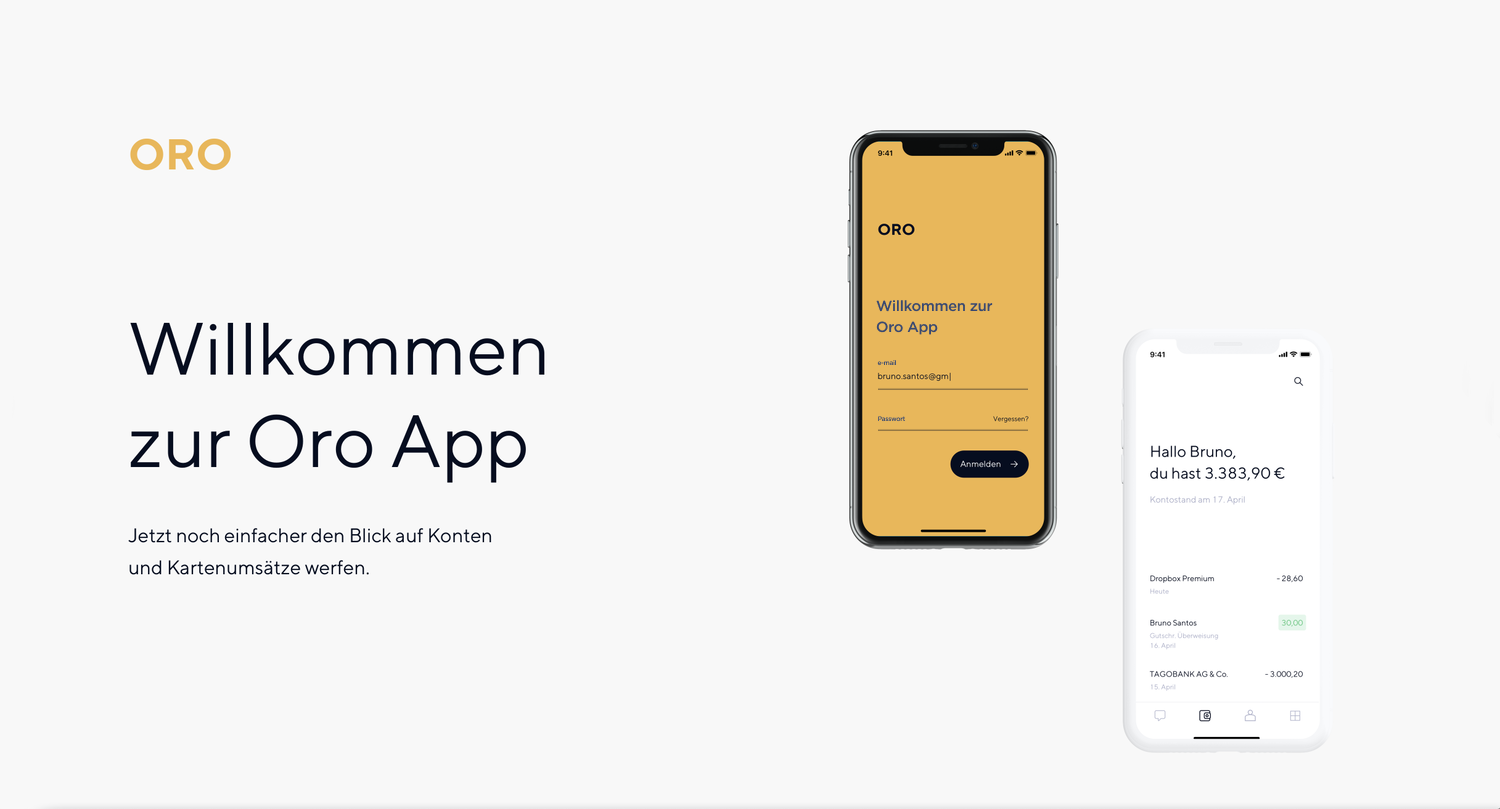

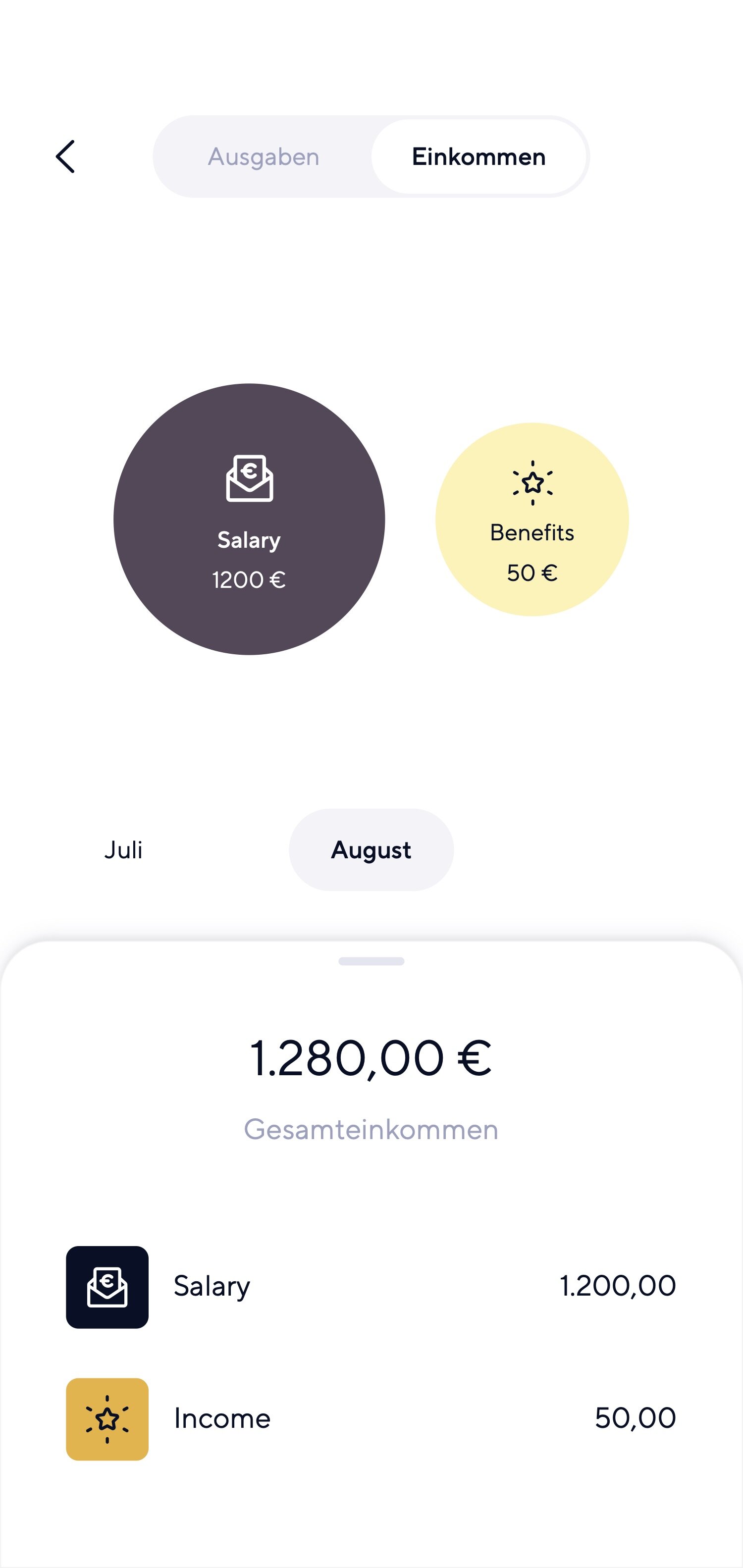

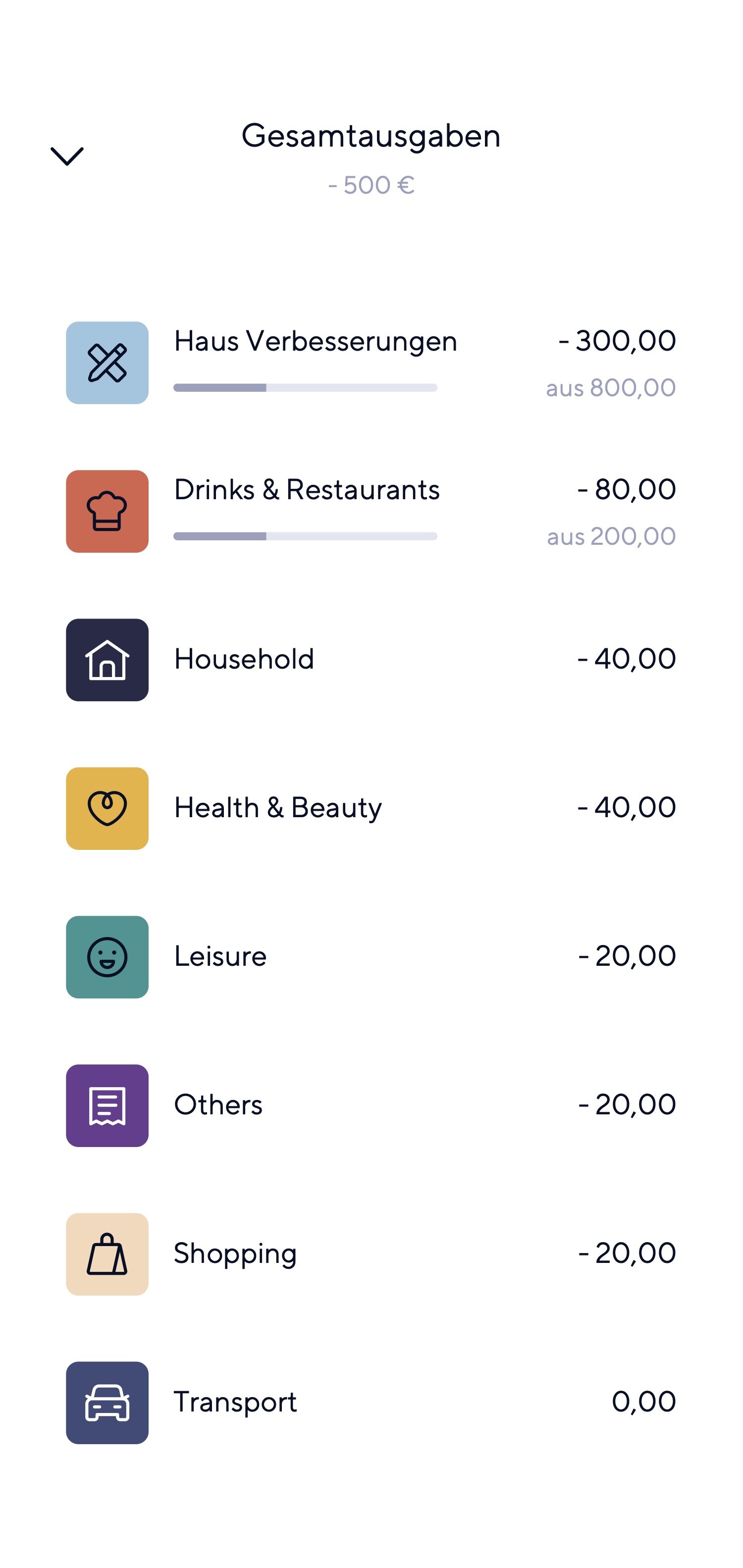

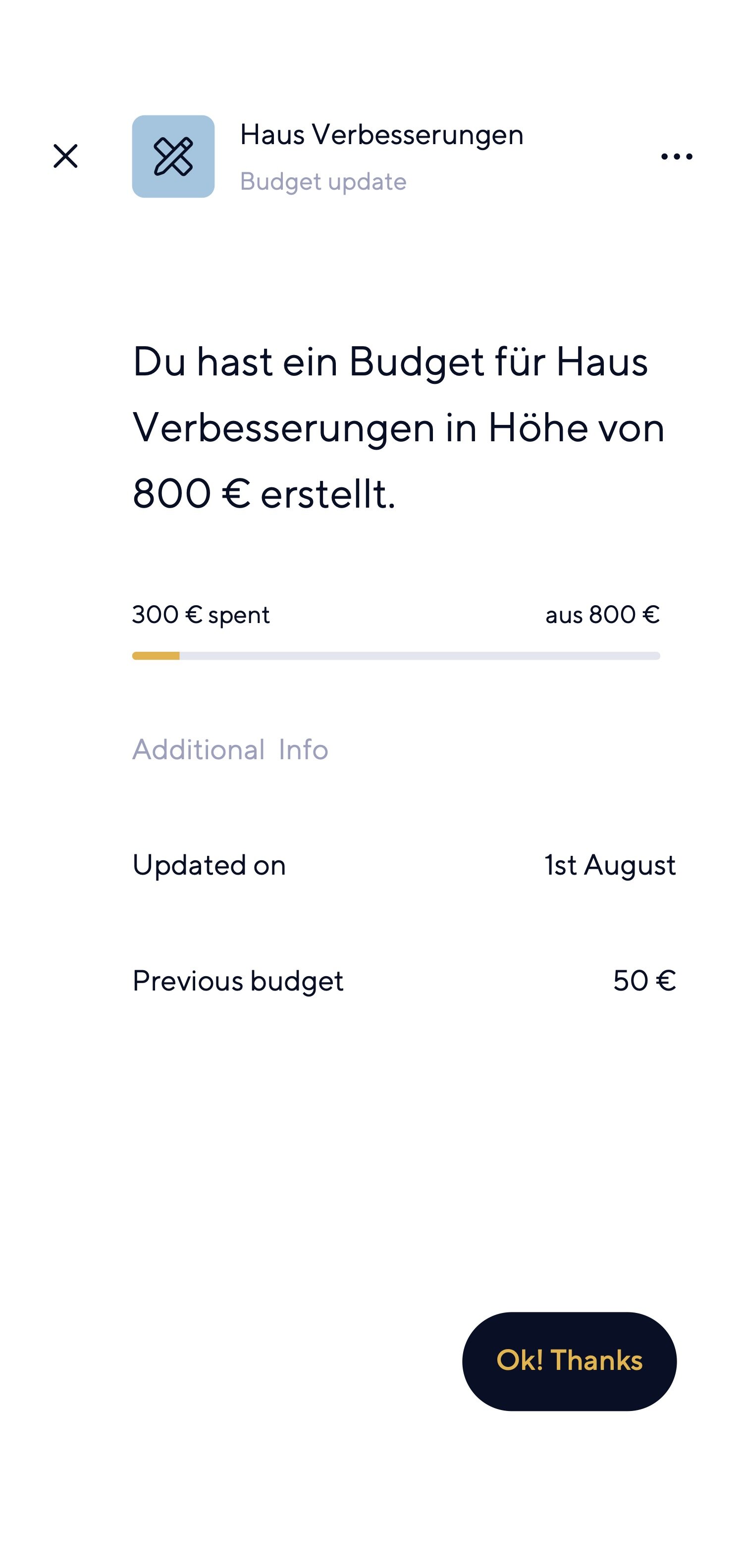

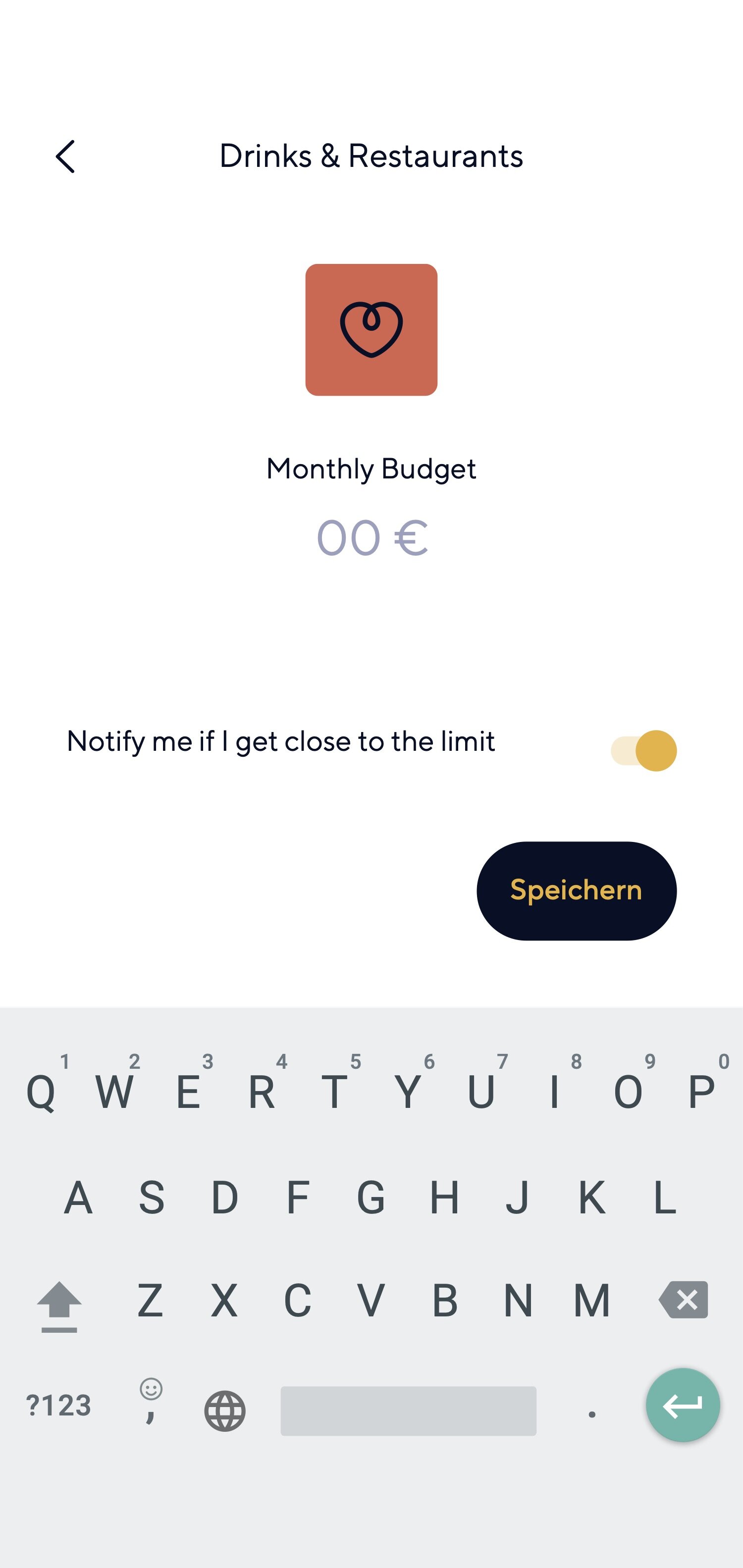

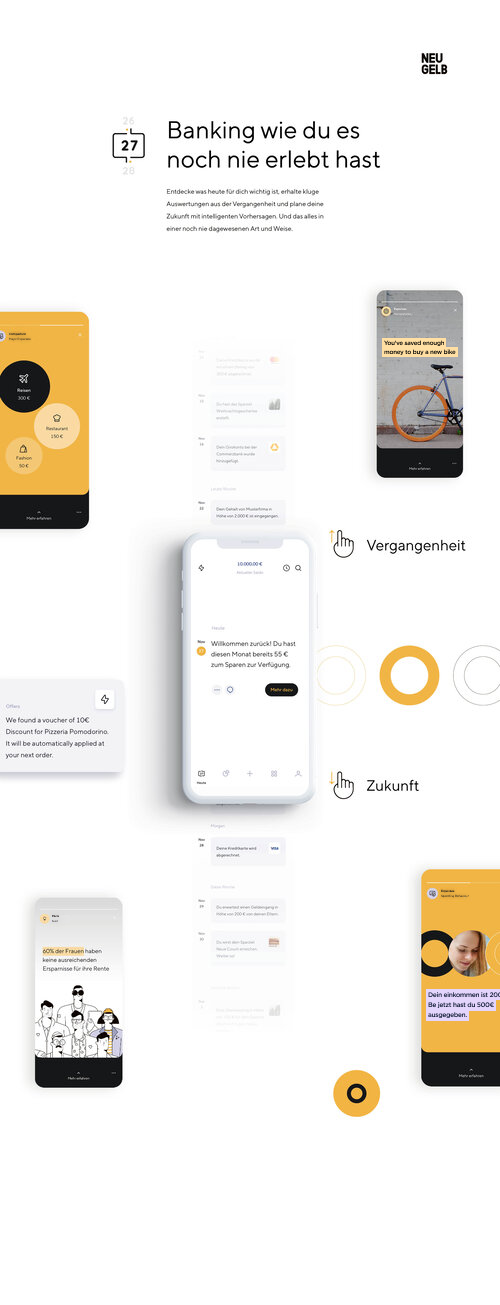

Spanish for ‘gold,’ Oro was thus designed to accommodate a younger audience of digital natives, intentionally sidestepping generic banking app conventions, traditional marketing strategies and static account updates. Linkable to any German bank account, Oro allowed users to set savings targets, track spending, and provided tips and insights about ways to optimise financial behaviour.

Oro combined a modern, minimalist visual style with money management, informative insight, educational resources and automation to make everyday banking as easy as possible for [German] Millennials.

Working closely with developers, strategists, stakeholders, UX researchers and other creatives, I analyzed research, data and product explorations to compile and share an Oro style guide.

This reference helped define personas, clarify visual language, finalize art direction, branding and identity. It also harmonized the design system, informing all UI decisions for designers and developers.

Together, we then refined and completed all MVP design features for the app in Q1 of 2020. User tests surpassed KPI’s, receiving very positive reviews and a high adoption rate, validating features, UI and UX.

Project Deep dive

PROBLEM 🤔

Whilst every incumbent bank had a digital solution for covering the basic needs of retail clients, there was no digital service that supported users to both understand their respective financial situation and receive personalized recommendations on how to improve it. Users had the following three sources available to build an understanding of / act upon their financial situation: Internet, Financial Advisor, and Friends & Family.

The internet holds an unlimited number of information on personal finance management and recommendations on all topics retail banking... however, this information is unstructured and not tailored to the user's individual situation and needs. It takes a long time to gather information and make sense out of it when applied to user finances. This manual process thus required substantial intrinsic motivation to keep it going over a long period of time to see any respective results.

A bank advisor presented one of the most traditional sources of knowledge on the topic of personal finance management. In this scenario, a user made an appointment at his/her respective bank, where the bank advisor collected all necessary information in order to shape recommendations based on the user's financial situation and goals. Unfortunately, this process was quite cumbersome for the user, as he/ she had to personally locate and visit a branch (and set aside time to attend appointments). Furthermore, the process required annual repetition (or if/when the personal situation of the user changed). Furthermore, any relationship built with the bank advisor would vanish were the bank advisor to leave a branch, or the user to relocate. Lastly, bank advisors were not available 24/7.

Friends and family were usually a trusted source for users when they needed advice on personal finance management. However, this input was not usually based on experience, deep nor formal financial knowledge. Also, people close to the user might not have had complete knowledge of the user's actual financial situation.

Each of these three described processes required full (or at least some) user intervention, and were difficult to maintain over a long period of time. Even if maintained and followed, users might have also missed out on important opportunities, due to a lack of knowledge or limited availability.

SOLUTION 💡

In order to address the drawbacks from available solutions, we came up with Oro. Oro aimed to take the complexity out of (everyday) banking by offering a fully digital and automated service to take over the user's finances. We achieved this by employing the most sophisticated technology (ie. artificial intelligence models, cloud infrastructure), and by making use of best-in-class third party providers.

Oro opted to cover all areas that retail banking comprises: service, saving, financing and investing. In order for the automation to kick in and find a high adoption rate, we found that building a trustworthy, transparent relationship between the user and Oro was of utmost importance. Hence, Oro followed the following process:

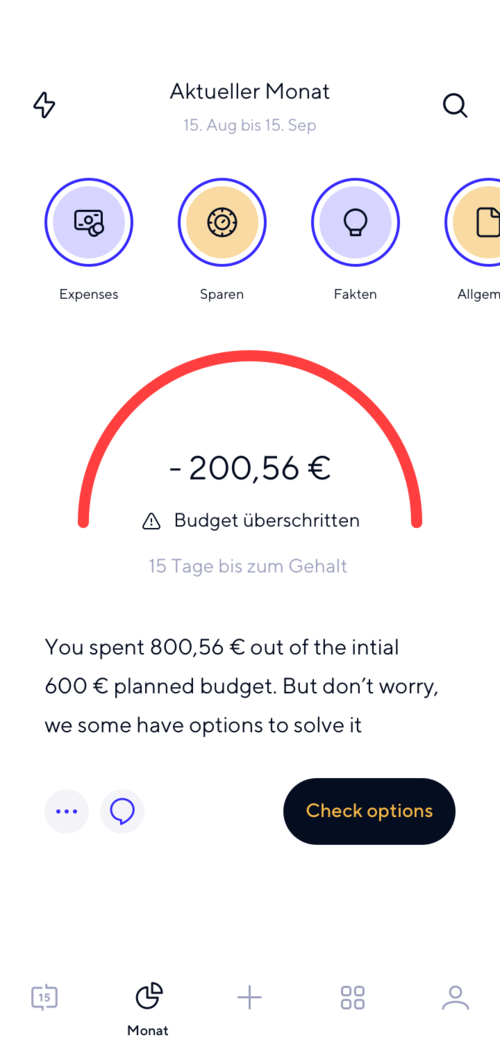

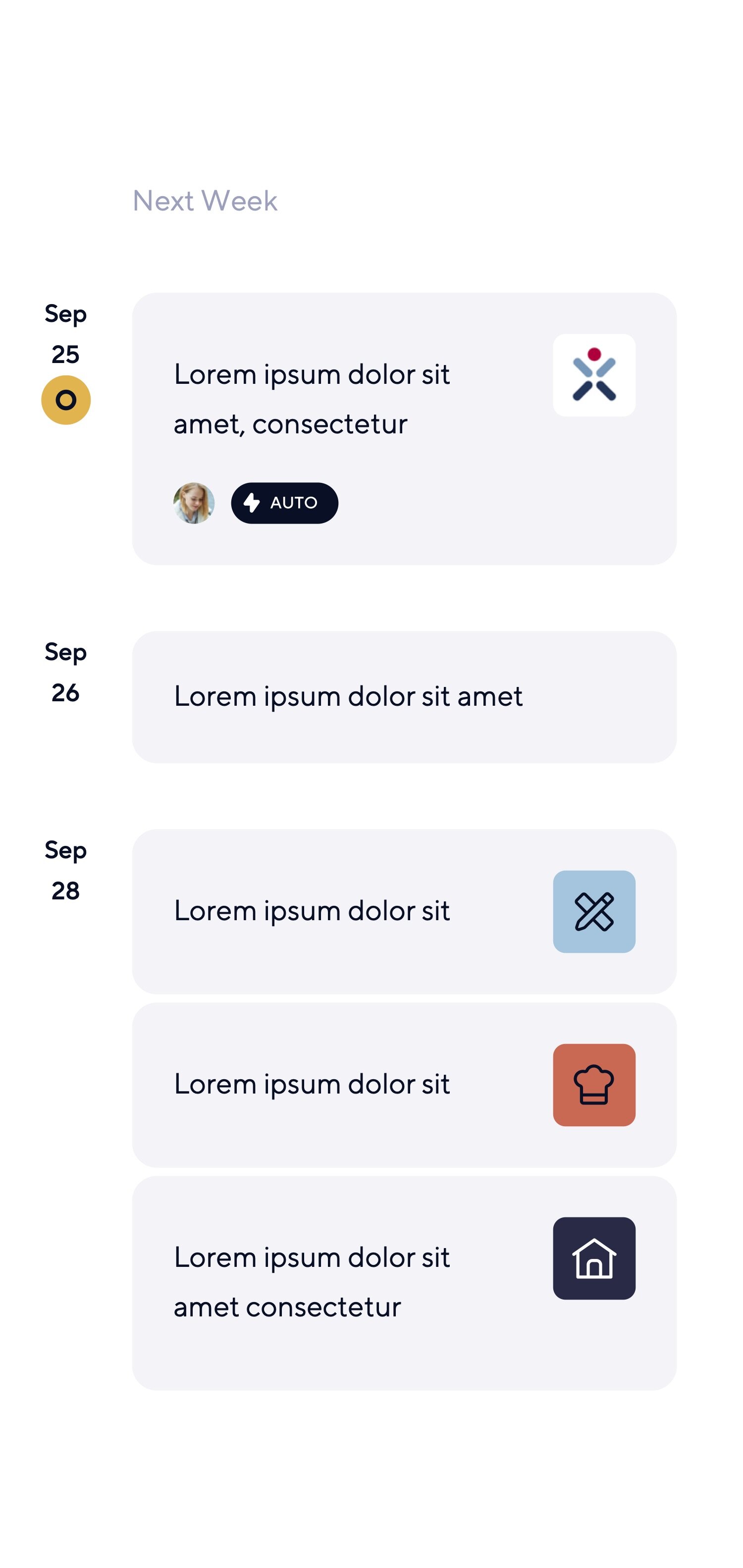

First, AI models, cloud infrastructure and third-party API’s supplemented service, saving, financing and investing areas. These technologies provided simplified behavioural insights, infographics, comparisons and advice for users to help them understand their financial situation.

Education became the second focus of Oro, helping users establish personal goals and learn how to responsibly fulfil them by optimizing their financial behaviour. These user-defined goals could be almost anything, from wishlist purchases and future trips to budgeting and forecasting expenses, saving up for a house, financing a vehicle and more.

As trust in the application grew over time, Oro would then suggest certain optimization actions for users. As an example, imagine Oro discovered that based on the current savings rates, a user would not be able to afford a previously-planned trip to New York. In order to increase the probability of achieving this goal on-time, Oro would recommend the user invest part of their savings into certain securities. Then, as the user realised the (financial) benefits that Oro unlocked, authorized automation would be suggested (and authorized) to simplify banking, realign user goals and make their digital banking experience as easy and effective as possible.

REsults

We were ambitious with the timelines, but the team was motivated and worked hard to overcome these challenges. Thus, the Oro app MVP was completed on time by our team at Neugelb in Q1 of 2020. Shortly before, Oro was granted an official German Banking License from the Federal Department for Financial Supervision of Germany (Bundesanstalt für Finanzdienstleistungsaufsicht, BaFin).

(This is no small feat!)

The German Federal Ministry of Finance in Berlin also expressed interest in collaborating with Neugelb on Oro. Representatives recognized the importance of proactively accommodating our identified user personas, and understood the value of a digital approach to promoting financial awareness and responsibility among modern German youth.

Statistically, Oro user tests surpassed project KPI’s*, receiving very positive reviews, high valuation and positive opt-in numbers. Linkable to any German bank account, Oro successfully allowed users to set savings targets, track spending, and provided tips and insights about ways to optimise financial behaviour.

*KPI’s:

User Engagement: measured recognition of product value, exploration of features and account linking/customized goal/budget setup by MVP testers

User Interest: 60% (or more) voluntary Beta sign-up/opt-in interest indication by MVP testers

User Trust and Retention: 30% quantifiable repeat user logins and goal/budget tracking by MVP testers (>5 repeat user logins per week over four weeks)

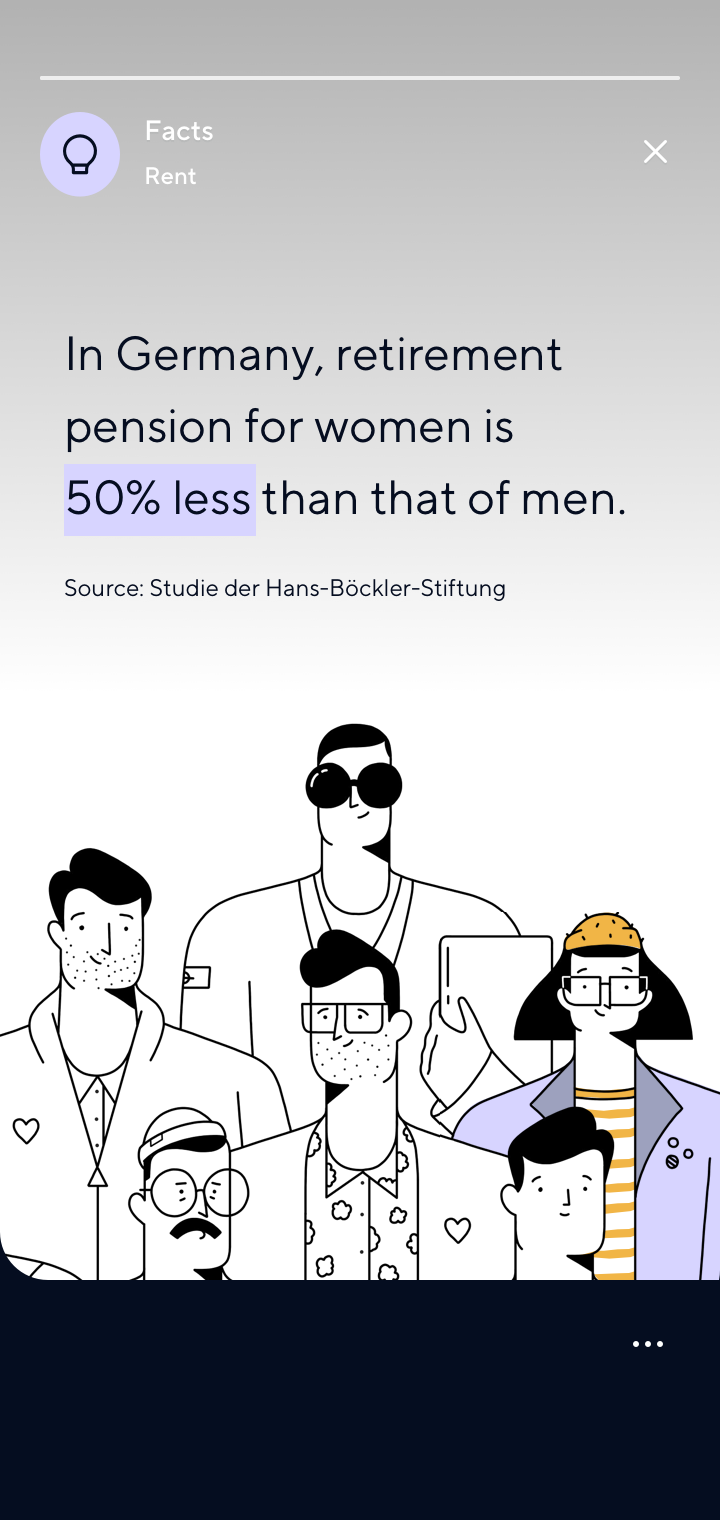

In addition to these points, UX research data and responses gathered during the Oro project also yielded interesting insights into German financial behaviours, history, biases, preferences, expectations and cultural values.

These insights were compiled and presented by UX Lead Tina Lickova at the 2020 UX Psychology Meetup in Berlin, Germany.

Presentation on ‘Insights into the financial psychology of Germans’ by Tina Lickova (Neugelb/Oro UX Lead) at the 2020 UX Psychology Meetup.

“Why we’re all weird about money” - a Medium article (and Q&A) by Kendall Anderson published on Jun 18 2020.

Financial Psychology and its implementation (PDF Presentation)